.png)

May 26th, 2026

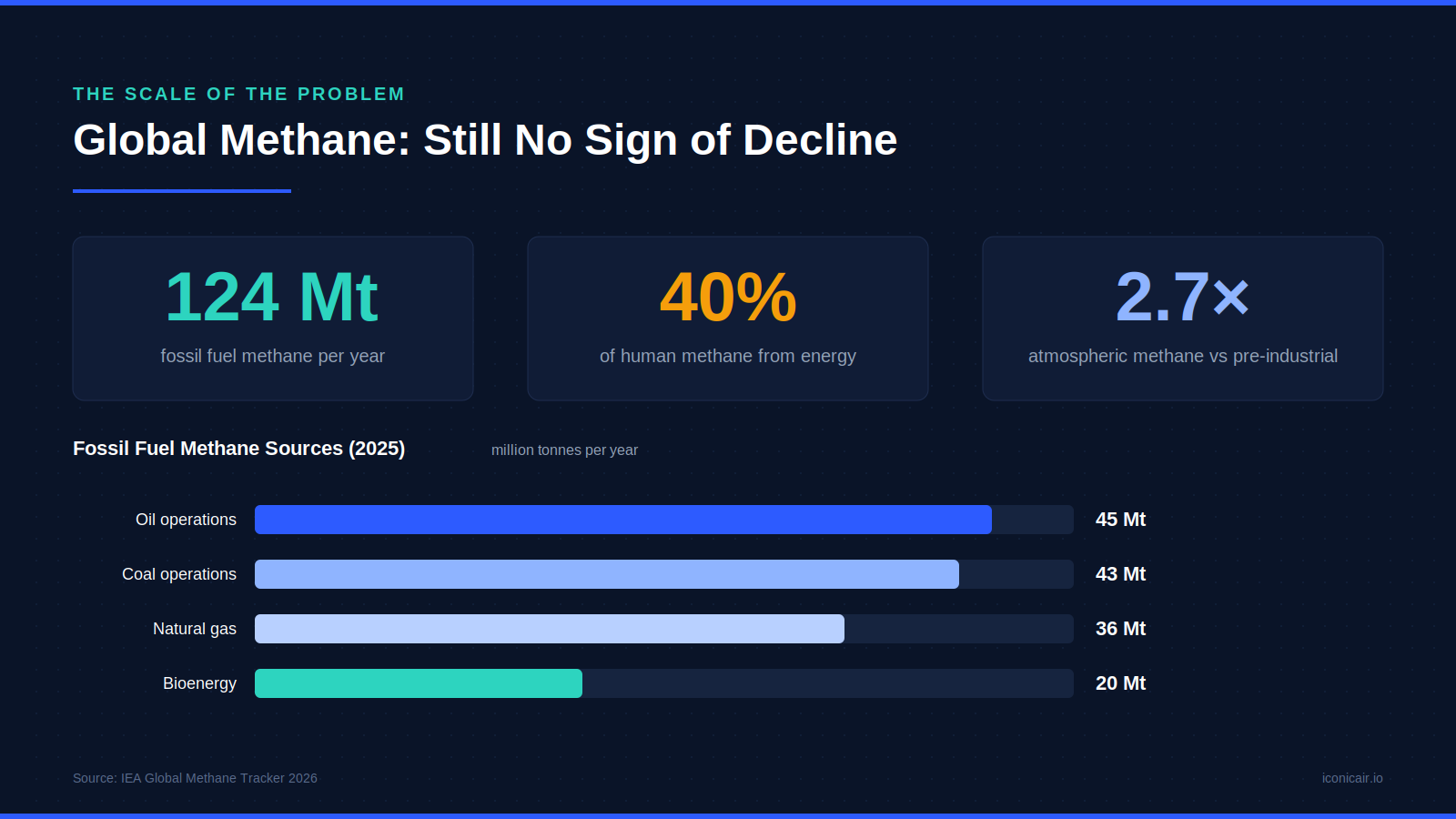

Every year the International Energy Agency publishes its Global Methane Tracker, and every year the industry expects the numbers to have moved. This year they didn’t - at least not enough. The 2026 edition, released in May alongside a G7 high-level event in Paris, confirmed that fossil fuel methane emissions are essentially flat at 124 million tonnes (Mt) per year, even as oil, gas, and coal production hit record highs in 2025. The gap between what the industry has pledged and what it has delivered has never been more visible.

For U.S. operators, that gap carries real commercial and regulatory consequences. This piece walks through what the data says, what the evolving regulatory landscape demands, and why the business case for action is stronger than most operators realize.

Atmospheric methane today sits at roughly 2.7 times its pre-industrial level and is responsible for nearly 30 percent of the rise in global average temperatures since the Industrial Revolution. That context matters because it underscores just how consequential the energy sector’s contribution is: the IEA estimates the sector emitted close to 150 Mt of methane in 2025, with fossil fuel operations alone accounting for 124 Mt of that total.

Breaking that 124 Mt down: oil operations are the single largest source at roughly 44-45 Mt, followed by coal at 43 Mt, and natural gas at 34–36 Mt. Bioenergy adds another 20 Mt on top. The headline is that despite well-known, proven, and often cost-negative mitigation pathways, global fossil fuel methane has not fallen. Pledges have multiplied. Action has not kept pace.

There is, however, a meaningful exception buried in the data: the global average upstream methane intensity of oil and gas production has fallen around 10 percent since 2019. Progress is possible. The problem is that it is uneven, and the worst performers drag the global average up considerably. Norway’s upstream intensity is more than 100 times lower than that of the worst-performing producers - a data point that functions less as a benchmark and more as an indictment of inaction elsewhere.

The United States is the world’s second-largest methane emitter from oil and gas operations, behind China. That ranking tends to surprise people who follow only domestic headlines, where U.S. performance is regularly compared favorably with Turkmenistan or Venezuela. That framing, while technically accurate, sets an extremely low bar.

The U.S. upstream intensity sits at roughly 0.6 percent — well below Turkmenistan’s 5-plus percent, and reflective of the improvement trend since 2019. But the Permian Basin, which accounts for a disproportionate share of U.S. production growth, remains a persistent hotspot. MethaneSAT data collected before the satellite lost contact in June 2025 found that Permian oil and gas operations were emitting approximately 440 tonnes of methane per hour, making it one of the world’s largest methane hotspots. The same dataset revealed striking regional variation within the basin: New Mexico operators emitted less than half the methane relative to production compared with their counterparts across the state line in Texas.

That variation matters because regulators and trading counterparties are no longer looking at national averages. They are looking at facility-level data. The satellite infrastructure to support that scrutiny now exists, even if individual missions come and go.

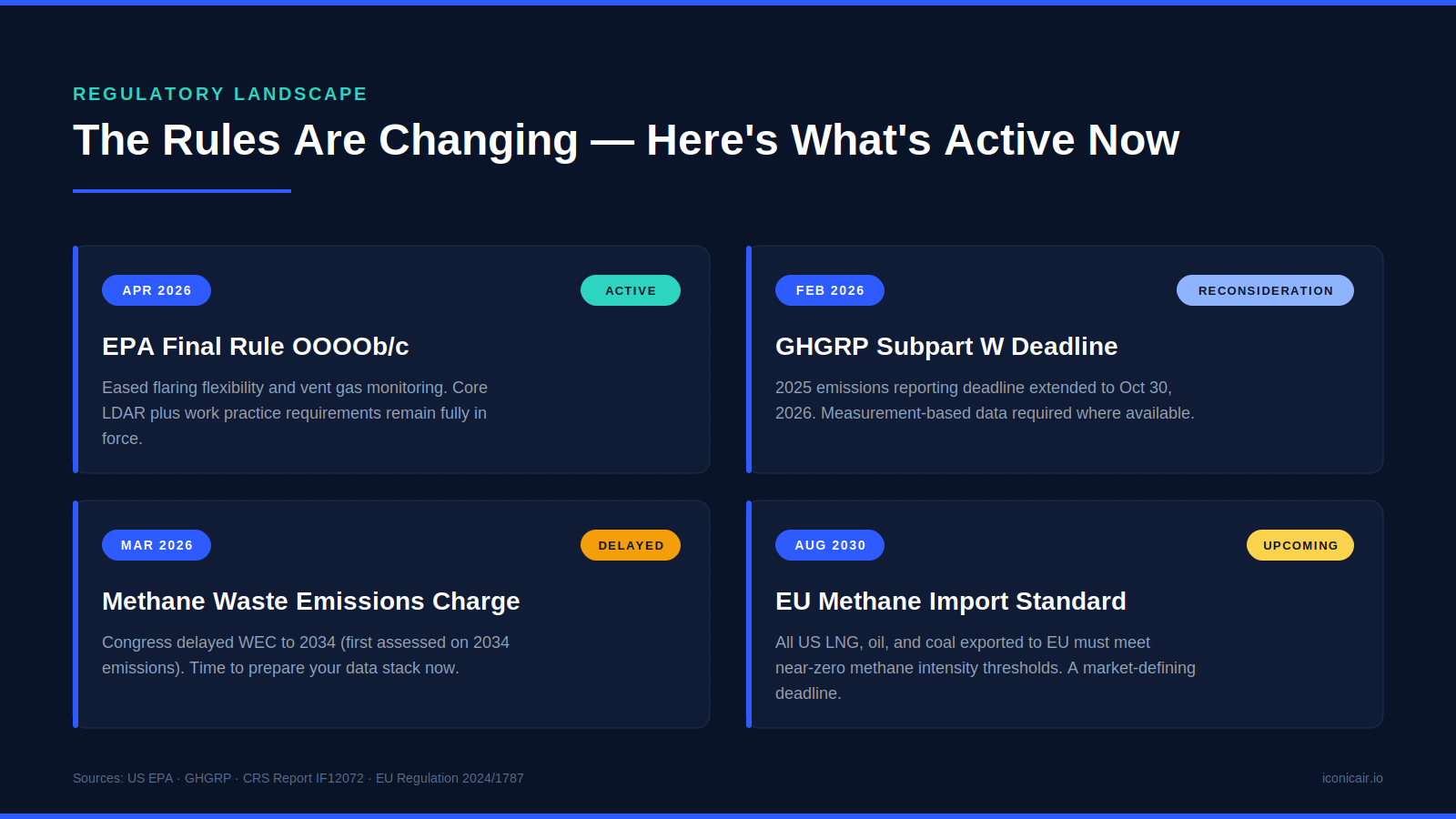

Three regulatory developments deserve close attention in 2026:

On April 4, 2026, the EPA finalized a reconsideration of two narrow aspects of its 2024 methane rules for oil and gas — specifically, temporary flaring provisions for associated gas and the continuous monitoring requirements for vent gas net heating value. The agency framed these changes as reducing regulatory burden and estimated savings for industry of approximately $2.5 billion between 2024 and 2038.

What has not changed: the core LDAR (leak detection and repair) requirements, the work practice standards, and the super-emitter program obligations under OOOOb remain in force. Operators who read the April 2026 rule as a green light to stand down on emissions management are misreading the regulatory direction of travel. The broader reconsideration of OOOOb and OOOOc announced in March 2025 is still ongoing, but even a substantially relaxed domestic rule does not eliminate the international market exposure discussed below.

The deadline for submitting 2025 emissions data under GHGRP Subpart W has been extended to October 30, 2026. Subpart W now requires measurement-based data where it is available, moving away from the emissions factor calculations that have historically allowed operators to understate actual emissions. The extension is a window of opportunity, not a reprieve. Operators who use the next several months to build robust, measurement-based data systems will be in a structurally better position than those who scramble in September.

If there is a single regulatory development that should concentrate minds at the executive level, it is the EU’s methane import requirements under Regulation (EU) 2024/1787. The timeline is tightening incrementally:

The widely cited target of 0.2 percent upstream methane intensity, aligned with OGMP 2.0 Level 5 and the Oil and Gas Decarbonization Charter, has not been formally adopted as the EU threshold, but it is the benchmark that most buyers and analysts are using to assess supplier risk. U.S. LNG and crude exporters that cannot demonstrate performance near that level face a credible risk of contract renegotiation or displacement from EU markets, not from regulation alone, but from buyer preference backed by publicly available methane intensity data from 2028 onward.

The IEA’s 2026 analysis confirms a figure that should be far better known across the industry: more than 35 Mt of global methane emissions could be eliminated at no net cost, based on 2025 energy prices. This is because the capital and operating costs of abatement are lower than the market value of the gas captured. At current energy prices, which are under upward pressure from Middle East supply disruptions, the economics are even more attractive.

Put differently: a significant portion of the methane the oil and gas industry is emitting represents revenue walking out the door. Upstream abatement alone could unlock close to 100 billion cubic meters (bcm) of additional gas supply annually. Eliminating non-emergency flaring could free up a further 100 bcm. That is a combined gas supply opportunity larger than Germany’s entire annual consumption.

Eighty percent of oil and gas methane comes from upstream operations (extraction, gathering, and processing). That is where abatement dollars go furthest. The IEA’s modelling suggests that full upstream abatement could cut global oil and gas methane intensity to below 0.2 percent, from roughly 1 percent today. The tools to get there are not experimental: LDAR programs, pneumatic device replacements, vapor recovery units (VRUs), and associated gas utilization are all commercially mature technologies.

The satellite methane monitoring ecosystem has matured rapidly and is now deeply embedded in regulatory and market infrastructure. TROPOMI, aboard the ESA’s Sentinel-5P, provides daily global coverage and detects the largest super-emitter events (above roughly 1 tonne per hour). GHGSat’s constellation, which signed a major partnership with ExxonMobil in September 2025 and is expanding toward nine satellites by end of 2026, offers facility-level point-source detection. Carbon Mapper’s Tanager-1 provides high-resolution attribution data. And UNEP’s Methane Alert and Response System (MARS), which draws on more than 35 satellite instruments combined with AI, notifies countries and operators of actionable emissions events in near-real time.

As of early 2026, 24 countries and nine subnational governments have designated formal “focal points” to receive MARS alerts directly. The IEA’s analysis found that if all countries mitigated MARS-notified super-emitter events within 30 days of the first alert, global oil and gas methane would fall by approximately 6 Mt per year which is equivalent to eliminating all upstream emissions from the entire Caspian region.

The loss of MethaneSAT in June 2025 was a setback for basin-level monitoring, but it did not meaningfully reduce the overall surveillance capacity. The data it collected, including the Permian Basin findings, continues to inform regulatory analysis and IEA estimates. New satellite capacity is being deployed. The monitoring infrastructure is not going away, and the EU’s methane regulation explicitly envisions satellite-based monitoring as part of its compliance architecture.

For operators, the practical implication is this: slow or non-existent responses to super-emitter events are now documentable and attributable. Regulatory bodies, trading counterparties, and ESG analysts can access that documentation. Response time has become a proxy for operational quality.

Commitments to cut methane now cover more than 55 percent of global oil and gas production, up from 20 percent at the time of the Glasgow COP in 2021. The Global Methane Pledge has drawn 159 countries. The Oil and Gas Decarbonization Charter (OGDC), signed by 56 companies, carries a near-zero methane target. OGMP 2.0 has become the industry gold standard for measurement and reporting, with Level 5, the highest tier, requiring source-level measurement and third-party verification, now the benchmark that the EU’s import rules will effectively demand.

Less than 10 percent of global production is now covered only by voluntary pledges without associated government requirements. That shift from voluntary to mandatory is significant. It means that for an increasing share of the market, methane performance is a compliance matter, not a reputational one.

Operators that are still treating methane management as a public-relations exercise rather than an operational and financial imperative are falling structurally behind. The companies that will win LNG offtake contracts in 2028 and 2030 are the ones building verifiable, measurement-based emissions data systems today.

The following is not a wish list. Each item is grounded in the specific regulatory and market pressures outlined above.

The 2026 IEA data delivers a clear verdict: the implementation gap between methane ambition and methane action remains large, but the tools, the economics, and the regulatory architecture to close it are all in place. For U.S. operators, the domestic regulatory environment may feel more permissive than it did two years ago. But the market environment - shaped by satellite surveillance, EU import requirements, and the growing premium on verifiable low-methane supply - is tightening in ways that domestic rule changes cannot offset.

Methane management is no longer a compliance checkbox. It is an operational discipline that directly affects revenues, market access, and license to operate. The companies that treat it that way today will be the ones writing the contracts in 2030.

Sources

We're excited to show you how Iconic Air can help your company mitigate climate risk and ensure access to capital.

Schedule a Demo